Key findings are powered by ChatGPT and based solely off the content from this article. Findings are reviewed by our editorial team. The author and editors take ultimate responsibility for the content.

A defined benefit plan is an employer-sponsored retirement plan that provides qualifying employees with a guaranteed payout in retirement. It's an alternative to a defined contribution plan, which gives employees more control over account contributions but requires them to take on more risk and doesn't provide a guarantee of a certain payout.

Defined benefit plans have fallen out of favor because they are more costly for employers. However, you can still find them with public agencies, government jobs, and some for-profit companies. Here's a closer look at how this type of qualified retirement plan works and how it stacks up to the more common defined contribution retirement plans.

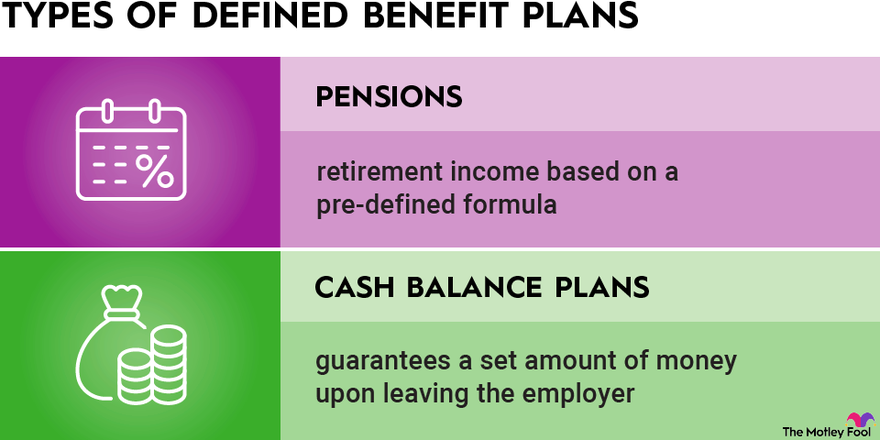

There are many types of defined benefit plans. They include:

Employers take on the investment risk with defined benefit plans, as well as the responsibility for making and managing employee contributions. These plans substantially differ from defined contribution plans such as 401(k)s, which do not guarantee employees will receive any set amount of funds upon retirement. A lifetime income guarantee makes defined benefit plans desirable for employees but risky for employers.

Every defined benefit plan will have its own formula for calculating benefits. However, one common formula involves employers paying a set dollar amount, such as $100 per month in pension funds, for every year an employee worked for the company. That would mean an employee who retires after working for 10 years would receive $1,000 in monthly benefits from the pension plan.

Your employer could also base your payout on your average income during your time of employment. If you earned $50,000 per year, or about $4,167 per month on average, and your pension plan says it will pay you 20% of your average monthly income, you would get about $833 per month.

Defined benefit plans don't usually require employees to contribute any funds to the plan. Instead, they are funded by the employer. However, some defined benefit plans may have voluntary or required employee contributions. Since employers manage and make contributions, they get to decide who qualifies for the plan and when and how you receive your payout -- but they must operate within U.S. Internal Revenue Service (IRS) and ERISA, or Employee Retirement Income Security Act of 1974, guidelines.

Pension plans can have vesting schedules, just like 401(k)s or other employer-sponsored retirement plans that offer matching contributions. If you leave your job before you're fully vested in the plan, you'll forfeit some or all of your pension.

Each company sets its own vesting schedule. However, if you don't think you're going to be with your employer for more than a few years, you may get more benefit from a 401(k) than you would from your company's pension plan. That's because you could contribute to your 401(k), invest the funds, and take your account balance with you after leaving (minus any employer matching contributions that hadn't yet vested).

You typically can't withdraw funds from your pension plan before you turn 65, but the exact age you may begin distributions will vary by plan. Some plans permit participants who are not yet eligible for distributions to take loans from their pension plans if they're in need of cash, but, just like with 401(k) loans, it's up to each individual employer to decide whether to allow this.

Your employer also dictates how it distributes benefits to you, within IRS and ERISA guidelines. Most pensions provide a regular monthly payment for the rest of your life. This is similar to an income annuity that offers a guaranteed monthly income, but the money comes from an employer rather than from an insurance company.

However, some employers give employees a lump sum instead. You may owe taxes on distributions, depending on how your plan is structured, so a lump sum might not be the most desirable payment method because it could raise your tax bill considerably for that year.

Your employer should provide you with details about these and other important pension terms so you know what to expect. If you have any questions about the plan, direct them to your company's HR department.

There are some significant benefits of defined benefit plans for employees:

There are also some disadvantages:

Defined benefit plans provide a predetermined payout. Defined contribution plans require or permit employees, and sometimes employers, to make contributions up to an annual limit. The actual payout in retirement depends on how much participants choose to contribute and how their investments perform. Common types of defined contribution plans include the 401(k) and the 403(b).

Defined contribution plans shift more of the savings burden to the employee, and that makes these types of retirement accounts less risky and less expensive for employers. That's why we've seen defined contribution plans rise in popularity over the past few decades while defined benefit pension plans have fallen out of favor.

Employers may still contribute money to defined contribution plans, but this often takes the form of a company match, where the employer will only contribute money if the employee does so first. Even then, employers will generally only contribute up to a certain amount.

Both types of plans can help you save for retirement, and some employers may enable you to have one of each so you can make personal contributions to your defined contribution plan while your employer contributes to your pension plan.

Whichever type of plan you are offered at work, make sure you understand all of its rules so you can get the most out of it. If your company offers a pension plan, ask about how it calculates your payout, its vesting schedule, and whether you'll receive money as a lump sum or a monthly payment so you can plan accordingly.

This specific type of retirement plan confers tax benefits to employees and employers.

Learn how, why, and how much to save for your golden years.

You've worked hard to build a retirement nest egg. Here's how to make the most of it.

We offer seven key steps to an early and comfortable retirement.